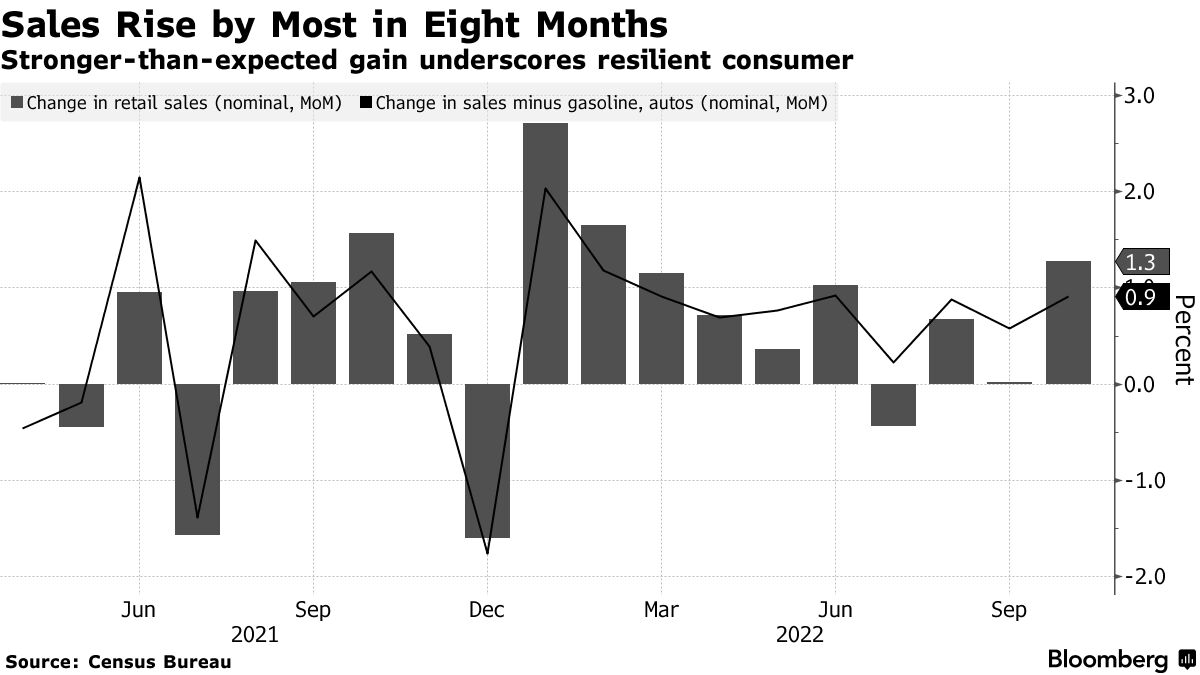

Despite concerns raised by executives from major American retailers about dwindling sales and consumer restraint, the US economy’s vitality remains intact, albeit undergoing a shift in consumer preferences. The surge in consumer spending that played a pivotal role in bolstering the economy during the pandemic continues, but it’s now directed towards different experiences and activities.

Evolving Consumer Appetite:

The narrative of consumer frugality propagated by certain retail leaders isn’t the whole truth. The inclination of consumers to spend remains robust; however, their preferences have evolved towards seeking novel experiences. This shift has led to a decline in purchases of traditional goods and a noticeable uptick in spending on events like concerts, travel, and leisure activities.

Exploring the Earnings Season:

During this earnings season, retail giants have cited various reasons for profit declines. Macy’s pointed to a rise in credit card delinquencies, potentially indicating strain among consumers. Dick’s Sporting Goods expressed concerns about shoplifting affecting margins. Foot Locker and Nike have faced declines in their stock values. Meanwhile, sales slumps have impacted retailers like Target, Home Depot, and Lowe’s.

Stable Economic Outlook:

However, these indications might not necessarily signify a dire economic downturn. Despite a reduction in spending on goods and the gradual depletion of Covid-era stimulus savings, overall consumer spending is far from stagnant.

Shift to Experience-based Spending:

Instead of acquiring more material possessions, consumers are channeling their discretionary funds into experiences like live events and travel. This transition is particularly noteworthy given that consumer spending contributes to a significant portion of the US gross domestic product (GDP).

Promising Economic Growth:

While the third-quarter economic growth rate won’t be officially revealed until late October, optimistic forecasts are emerging. According to Chris Rupkey, Chief Economist at FwdBonds, predictions for GDP growth are “running wild on the upside.” The unofficial GDPNow forecast from the Atlanta Federal Reserve suggests a substantial 5.8% annualized growth rate in the third quarter, double the rate from the same period last year.

The Notion of Fatigue, Not Strain:

A key observation made by Bloomberg columnist Leticia Miranda is that consumers are experiencing fatigue rather than financial strain. This viewpoint aligns with the notion that the economy is still sound, but retailers need to invigorate consumers’ interest to counteract their current state of boredom.

Balanced Spending Approach:

Although consumers haven’t ceased spending altogether, their spending habits have become more measured due to the impact of inflation. This shift has particularly favored retailers like Walmart, Amazon, and TJ Maxx, which offer discounted items, leading to increased revenue during the second quarter.

Comparative Perspective:

It’s important to view retailers’ warnings about the state of the American consumer within the context of the pre-pandemic era. Historical correlations between sluggish retail sales, credit card delinquencies, and economic downturns might not be directly applicable in today’s context.

Positive Economic Factors:

Unlike past scenarios, the current economic landscape exhibits positive indicators. Wages are rising, inflation is cooling down, and unemployment has remained relatively low. These factors counteract the traditional warning signs associated with economic decline.

Nuanced View on Credit Card Debt:

The concern over rising credit card debt is nuanced. While delinquent debt has increased, it was virtually non-existent over the past few years, making the current elevation appear more significant than it might be. Rising credit card balances, to some extent, reflect consumers’ optimism about paying off their expenses in due time.

Challenges and Positives:

The economy isn’t devoid of challenges, as seen in increased credit card and auto loan debt and a decline in savings. The upcoming reintroduction of student loan payments also poses a challenge. However, the momentum driving the economy seems to be more resilient in the face of these challenges, suggesting the potential for it to navigate these headwinds.

Conclusion:

While the dynamics of consumer spending are evolving, the US economy’s core remains robust. The transition from material goods to experiences marks a shift rather than a decline. As the economy adjusts to changing consumer preferences, the resilience displayed against potential challenges reflects a promising outlook for the nation’s economic trajectory.